ASX Giants vs. Global Challengers: A 2026 Snapshot

In a dynamic economic landscape, investors are constantly seeking opportunities that offer robust returns and sustainable growth. In 2025, an insightful exercise was conducted, pitting some of Australia’s leading companies against their international counterparts operating in similar sectors. The objective was not to declare outright victors, but to conduct a side-by-side comparison of fundamental metrics – valuation, profitability, growth, and capital allocation – to discern where the numbers pointed. This analysis proved remarkably instructive, frequently highlighting that companies trading at more sensible valuations with stronger operating performance often outperformed their pricier rivals, particularly when underpinned by a credible expansion narrative.

This year, as 2026 unfolds, this comparative exercise has been revisited, aligning another cohort of ASX entities with global players to identify emerging investment prospects.

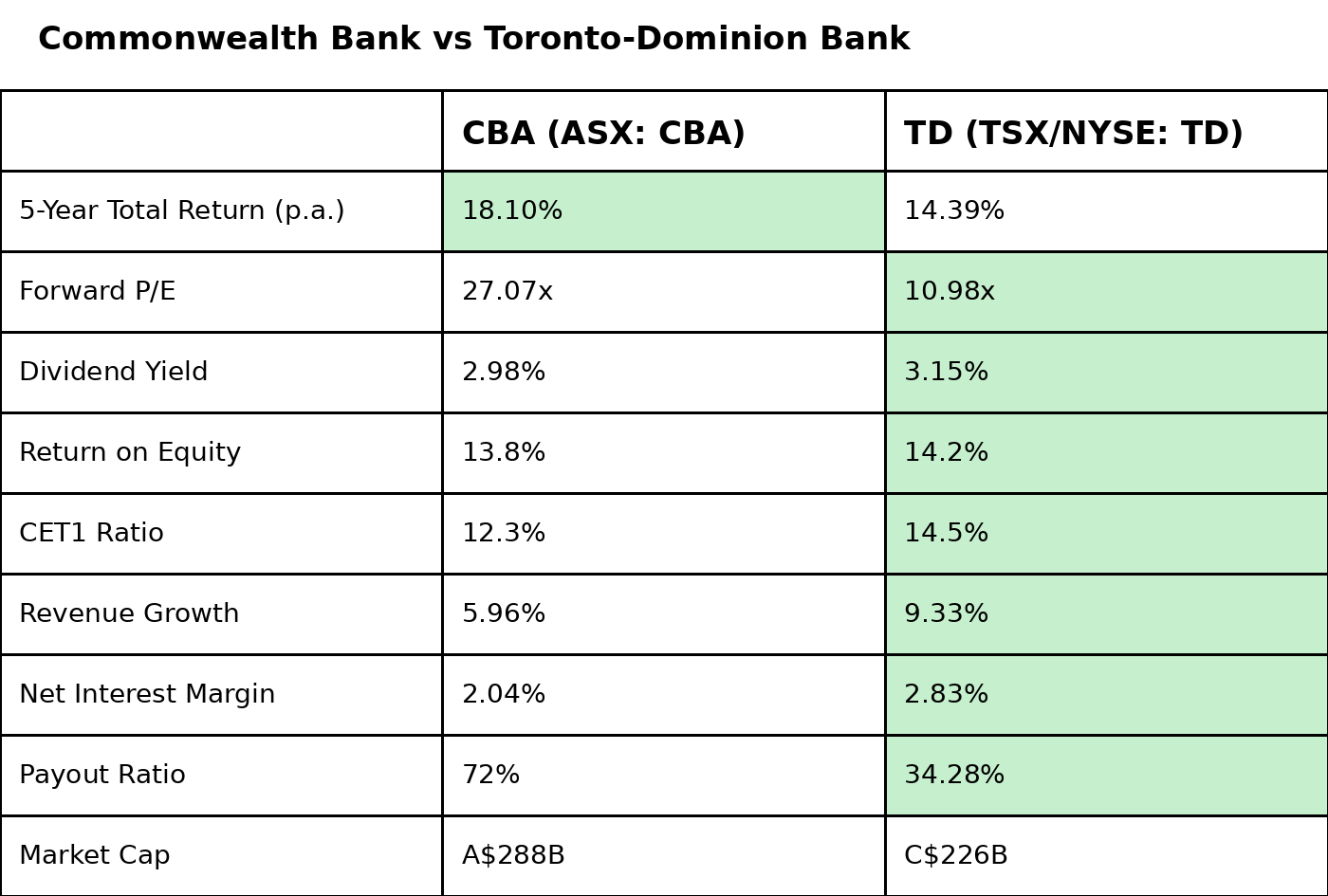

A Tale of Two Banks: Commonwealth Bank vs. Toronto-Dominion Bank

One of the most compelling comparisons emerges from the banking sector. For Australian investors accustomed to paying premium multiples for their domestic “big four” banks, the prospect of acquiring a similarly dominant financial institution at a mere 11 times earnings can seem almost unbelievable. It’s a valuation that Commonwealth Bank (ASX: CBA) is unlikely to reach anytime soon. However, a transatlantic hop could present an alternative: Toronto-Dominion Bank (NYSE: TD / TSX: TD). As Canada’s second-largest lender, TD benefits from many of the same structural advantages as Australia’s major banks, including robust population growth, a stable legal and economic framework, and a commanding presence in its home market.

On most fundamental indicators – valuation, capital strength, revenue expansion, and profit margins – TD presents a very favourable comparison to CBA. So, what accounts for the valuation disparity? TD faced headwinds for several years due to a US anti-money-laundering investigation, which ultimately resulted in a US$3 billion penalty. With this issue now resolved and a new CEO at the helm, TD has embarked on a path of operational simplification and cost reduction. Furthermore, the bank divested its US$13.1 billion stake in wealth manager Charles Schwab, with CEO Raymond Chun signalling an intent to utilise these proceeds for share buybacks, enhancing returns, and focusing on less risky organic growth strategies. Given its current valuation, a cleaner balance sheet, and potential catalysts for re-rating, TD warrants a prominent position on any investor’s watchlist.

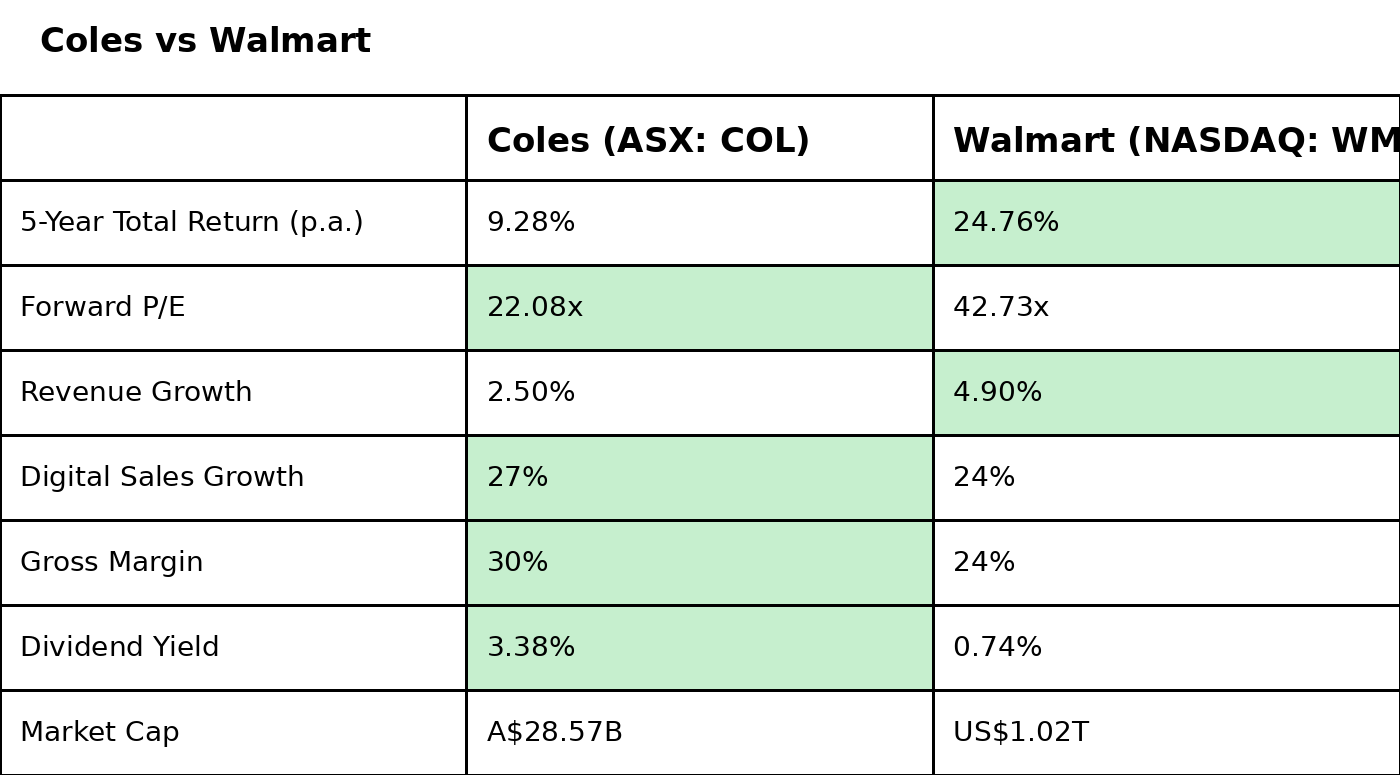

Supermarket Showdown: Coles vs. Walmart

For those familiar with North America, Walmart (NASDAQ: WMT) stands out as a retail titan that commands immense daily foot traffic. The company has cultivated a vast empire by catering to value-conscious consumers seeking a one-stop shop for everything from groceries to electronics. Yet, the stark valuation difference between Walmart and Australian retailer Coles (ASX: COL) presents an intriguing investment dilemma.

Walmart trades at a premium multiple despite experiencing relatively modest revenue growth. Investors appear to be banking on the company’s ability to transcend its traditional retail identity. Much of this optimism is tethered to its burgeoning online business, where it directly competes with Amazon. While Coles boasts a stronger e-commerce growth rate, Walmart operates within a significantly larger addressable market of American consumers. This enthusiasm has propelled its stock by approximately 30% over the past year, pushing its market capitalisation beyond the US$1 trillion mark. Coles, conversely, operates within Australia’s highly lucrative supermarket duopoly. Its profit margins remain robust, its dividend yield is more attractive, and its valuation is considerably more accessible.

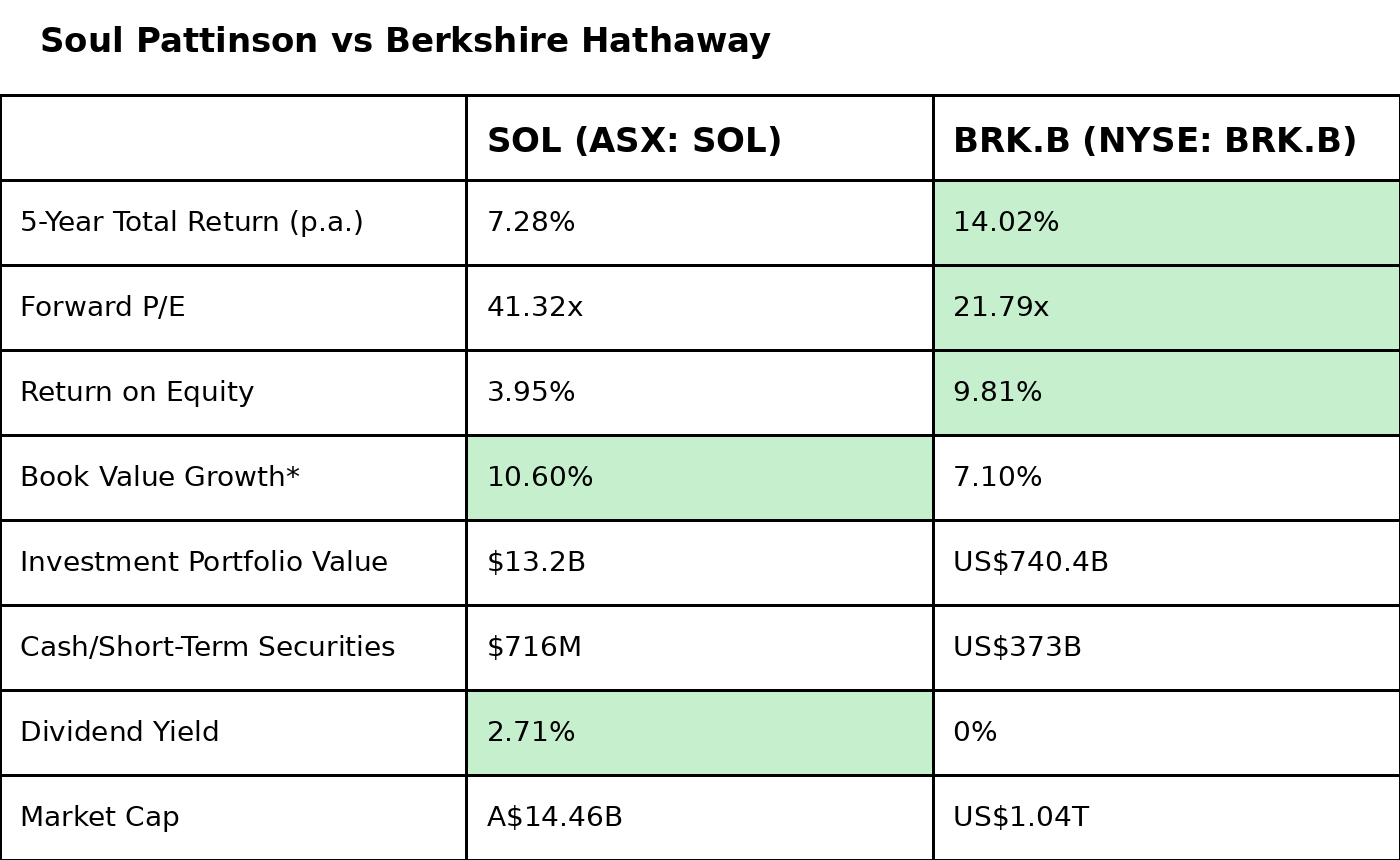

Investment Conglomerates: Soul Pattinson vs. Berkshire Hathaway

These two entities represent venerable investment houses within their respective markets. Soul Pattinson (ASX: SOL) is steered by CEO Todd Barlow, with strategic guidance from Chair Rob Millner, while Berkshire Hathaway’s vast conglomerate is managed by the legendary Warren Buffett and his successor, Greg Abel. Fundamentally, both companies function as sophisticated capital allocation vehicles, deploying shareholder capital across listed equities, private markets, and wholly-owned subsidiaries. Berkshire’s stable includes behemoths like BNSF Railway and GEICO, while Soul Pattinson holds stakes in diverse businesses ranging from building materials giant Brickworks to the aquatic education provider Aquatic Achievers Swim Schools.

Traditional financial metrics such as revenue growth are often less relevant for companies of this nature. The sale of a significant asset or equity holding can naturally distort earnings and cash flows in any given fiscal year. On a purely quantitative basis, Berkshire Hathaway appears stronger, generating superior returns on equity and trading at a lower valuation multiple, despite its vastly greater scale and financial capacity. However, Berkshire’s management has historically been reluctant to distribute dividends. Credit must be given to the teams at Soul Pattinson, led by Millner and Barlow. The company has demonstrated faster growth in its book value – representing the underlying worth of its assets and businesses – compared to its American peer, while also consistently increasing its dividend for over 25 years. The trade-off? Investors currently face a higher valuation multiple for this impressive track record. A potential deciding factor could be executive alignment: Greg Abel recently announced his intention to invest his entire US$15 million after-tax annual salary into Berkshire Hathaway shares. This level of shareholder commitment is a powerful indicator.

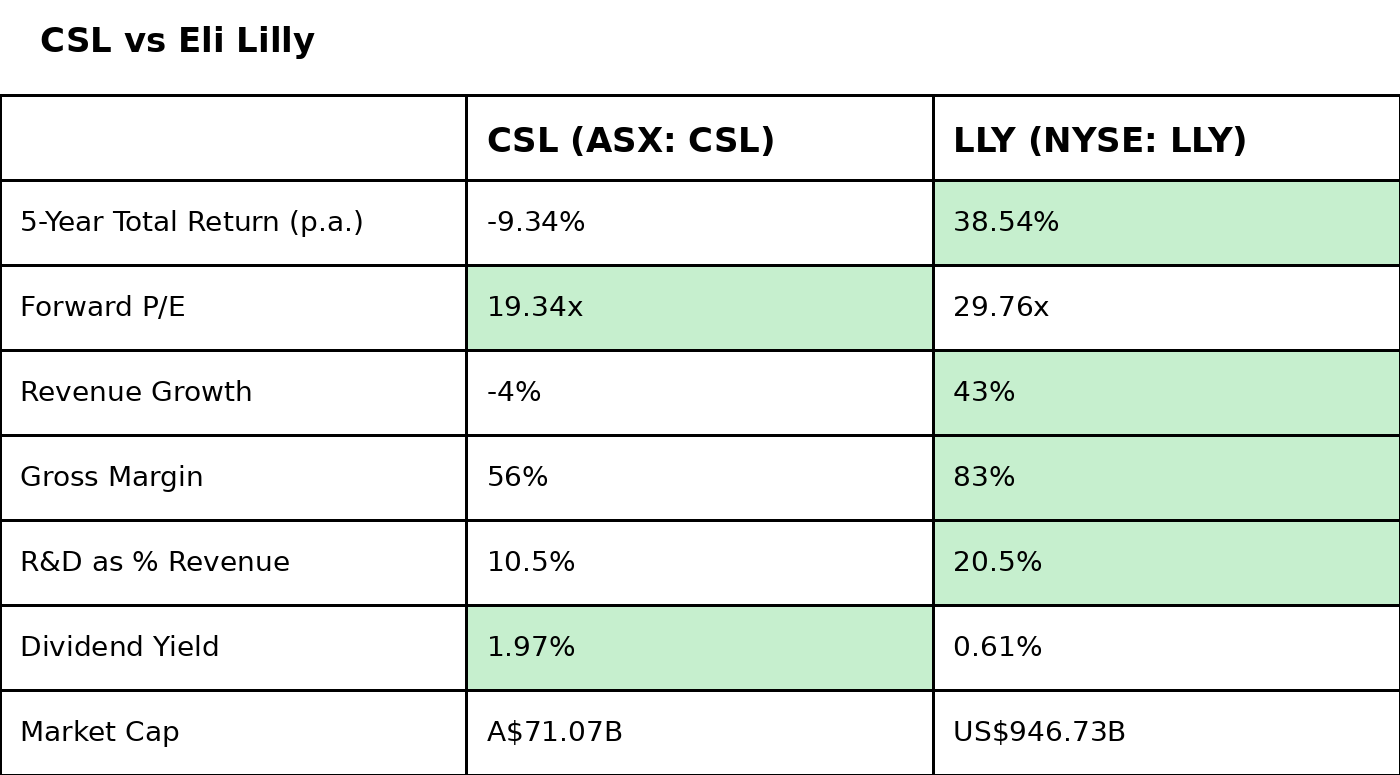

Biopharmaceutical Powerhouses: CSL vs. Eli Lilly

Few companies have made as significant an impact on global healthcare markets recently as Eli Lilly (NYSE: LLY). This pharmaceutical giant has emerged as a major beneficiary of the GLP-1 revolution, with its blockbuster weight-loss and diabetes medications driving revenue growth to unprecedented levels.

Eli Lilly also boasts exceptional profitability, with gross margins significantly exceeding those of CSL (ASX: CSL). Furthermore, it reinvests nearly double the proportion of its revenue into research and development. This substantial investment is fuelling a robust pipeline that spans obesity, oncology, immunology, and neurological disorders, with new oral GLP-1 treatments potentially broadening its market reach even further. CSL, while remaining a world-class biotechnology company with established leadership in plasma therapies and rare disease treatments, has experienced a slowdown in its growth trajectory in recent years. This has been attributed to post-pandemic disruptions in plasma collection, alongside more recent challenges related to management forecasts and strategic decisions.

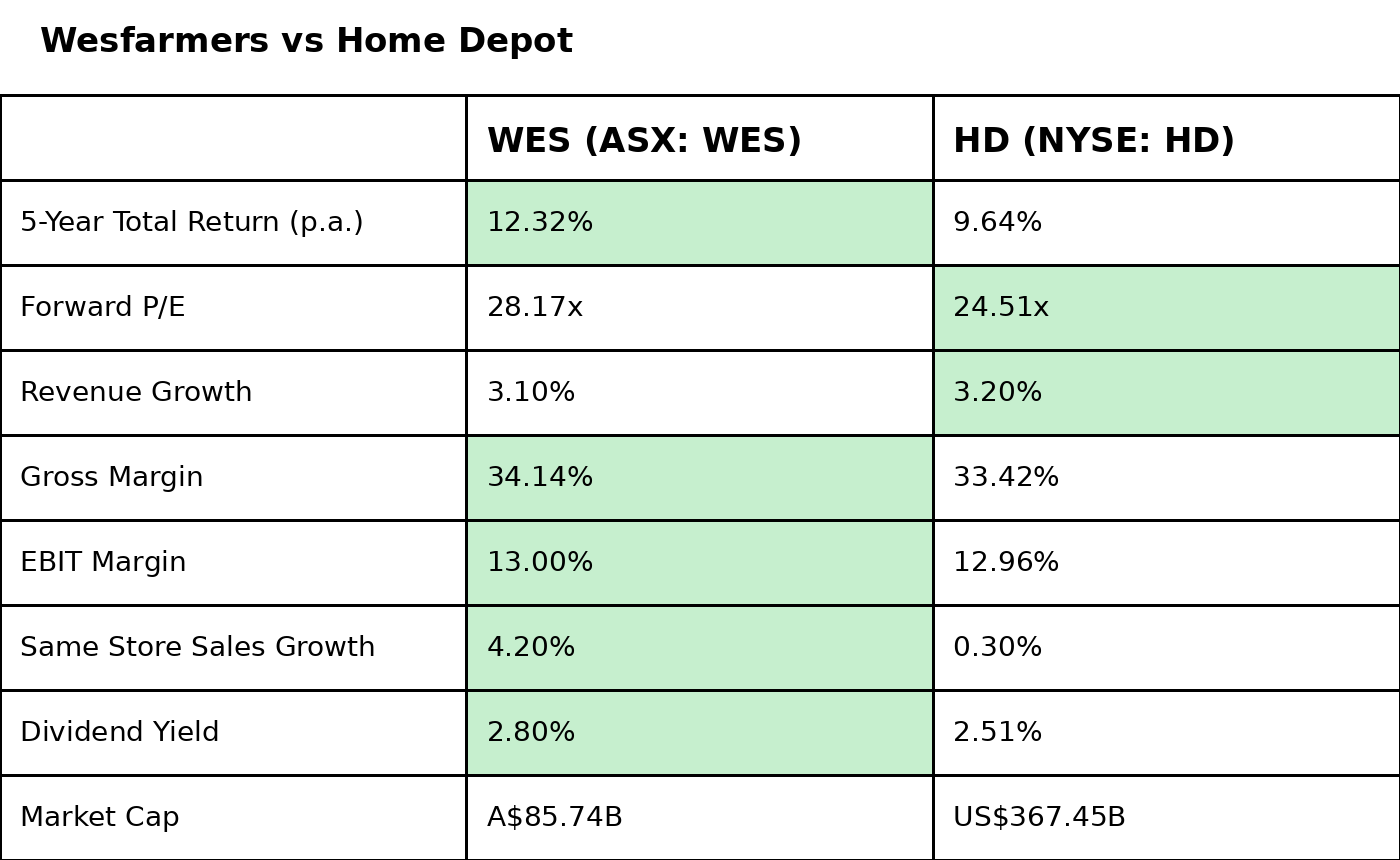

Diversified Retail vs. Home Improvement Specialisation: Wesfarmers vs. Home Depot

Both Wesfarmers (ASX: WES) and Home Depot (NYSE: HD) are distinguished retailers, yet their operational models diverge significantly. Home Depot operates as a pure-play home improvement giant, its fortunes closely intertwined with the cyclical nature of the North American housing market. Wesfarmers, on the other hand, is a diversified retail conglomerate with a broad portfolio encompassing Bunnings (home improvement), Kmart (discount department store), Officeworks (office supplies), and various healthcare investments.

Housing remains a national obsession in Australia, and the renovation and furnishing of these homes are core to consumer spending. Wesfarmers has masterfully capitalised on this trend.

On a quantitative level, Wesfarmers demonstrates an advantage over its American counterpart across most key performance indicators, most notably in same-store sales growth. This metric is crucial as it signifies that the business is not solely reliant on opening new stores for expansion; rather, it is successfully encouraging existing customers to increase their spending at current locations. In this particular comparison, the rationale for seeking opportunities offshore becomes less compelling.

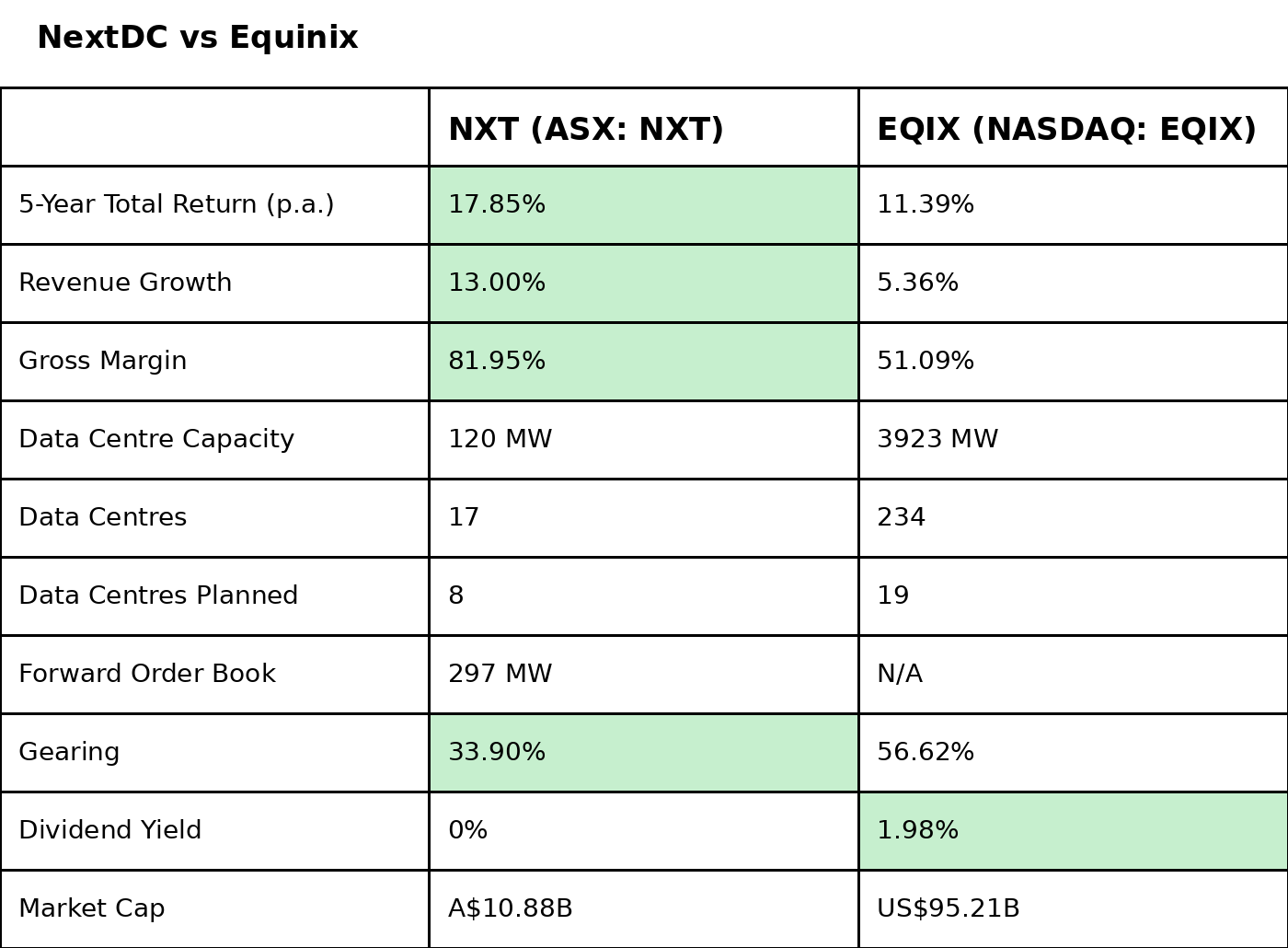

Data Centre Dominance: NextDC vs. Equinix

For those who contend that Australia lacks high-calibre technology infrastructure companies, NextDC (ASX: NXT) serves as a compelling counter-argument. The company has solidified its position as Australia’s premier data centre operator, capitalising on the global surge in demand for AI infrastructure and cloud computing capacity. We compare it to Equinix (NASDAQ: EQIX), the world’s largest data centre provider.

Certain metrics presented below – such as data centre capacity, the number of facilities, and planned new developments – are primarily included to illustrate the sheer scale difference between these two companies. However, sheer size alone does not guarantee success in this industry. Ultimately, the unit economics of asset operation are paramount. On this basis, NextDC appears to be outperforming its larger rival, exhibiting stronger revenue growth, superior margins, and lower financial leverage. It is important to note that these comparisons are not perfectly aligned. Equinix operates as a US REIT, which necessitates distributing a significant portion of its income to shareholders, whereas NextDC prioritises reinvestment into expanding its capacity. While NextDC is not yet profitable, it appears to be effectively leveraging the robust demand associated with the AI and cloud computing boom.

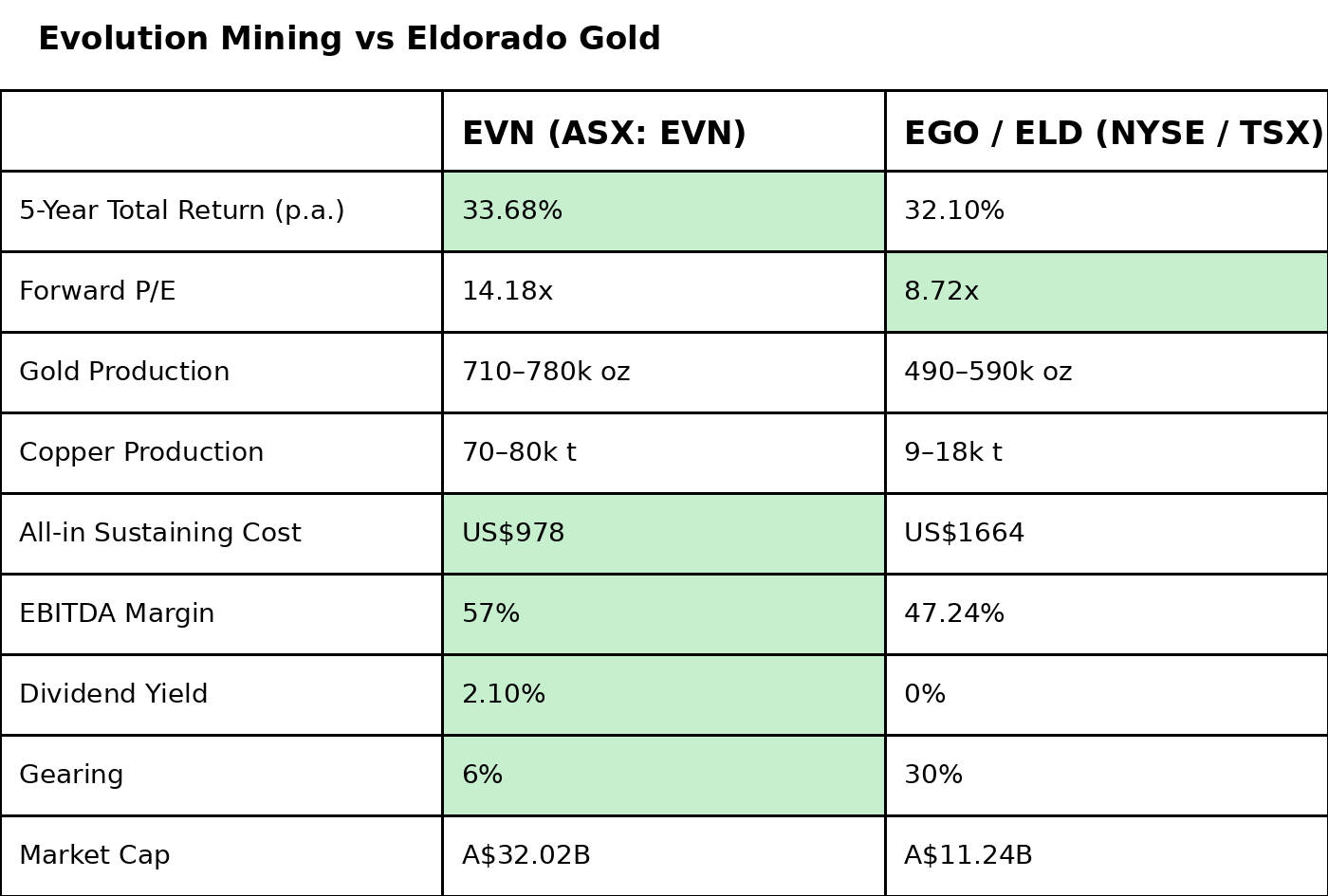

The Gold Standard: Evolution Mining vs. Eldorado Gold

Consider this the Winter Olympics of gold mining, featuring two formidable, albeit friendly, rivals: Australia and Canada. Evolution Mining (ASX: EVN) is a darling of the ASX market, having delivered exceptional returns by operating in opportune locations with desirable commodities – gold and copper. The company’s operations are primarily based in Australia, with the notable inclusion of the Red Lake mine in Canada. Eldorado Gold (NYSE: EGO / TSE: ELD), meanwhile, operates mines in Canada and Europe. Following a recent acquisition, it is set to incorporate the McIlvenna Bay project in Saskatchewan and Skouries in Greece, thereby significantly increasing its gold production and establishing a meaningful presence in copper. This strategic move brings the business mix of both miners into greater alignment.

If we focus solely on current financial metrics, Evolution Mining presents a formidable case. It extracts metals at a lower cost, generates stronger profit margins, pays a dividend, and carries minimal debt. However, it lacks a significant growth catalyst. Evolution is projected to produce roughly the same volume of gold and copper in FY26 as it did in the previous year. In contrast, thanks to its acquisition of Foran Mining, Eldorado Gold anticipates a roughly 40% increase in gold production by 2027, while also generating substantial revenue from copper for the first time this year. This comparison presents a challenging decision. Both companies appear to be strong contenders, provided the prevailing gold price remains supportive.

Leveraging Diversification for Investment Advantage

The overarching conclusion from these comparisons is not that global companies are invariably superior to their ASX counterparts. However, given that Australia represents a mere 2% of the global equity markets, investors who confine their portfolios to domestic listings may be overlooking some of the world’s most robust businesses or potentially more advantageous opportunities within the same sectors. Often, the most astute strategic move is not to completely divest from an ASX holding, but rather to question whether a superior version of that company exists elsewhere on the global stage. This is the significant advantage afforded to modern investors, with trading platforms increasingly providing cost-effective access to the world’s leading equity markets.

{kind=link}