Geopolitical Shockwaves Rock Markets: Energy Stocks Surge Amidst Middle East Tensions

The global financial markets have been jolted by a significant geopolitical event, sending shockwaves through energy sectors and causing widespread investor apprehension. Escalating tensions in the Middle East have triggered a sharp surge in oil prices, as traders grapple with the heightened risk of supply disruptions in a region vital to global energy production.

The market’s reaction has been immediate and pronounced. Oil prices have shot upwards, while equity markets worldwide have experienced considerable declines. Investors are now factoring in the implications of this new geopolitical flashpoint, leading to a rapid reassessment of risk across various asset classes.

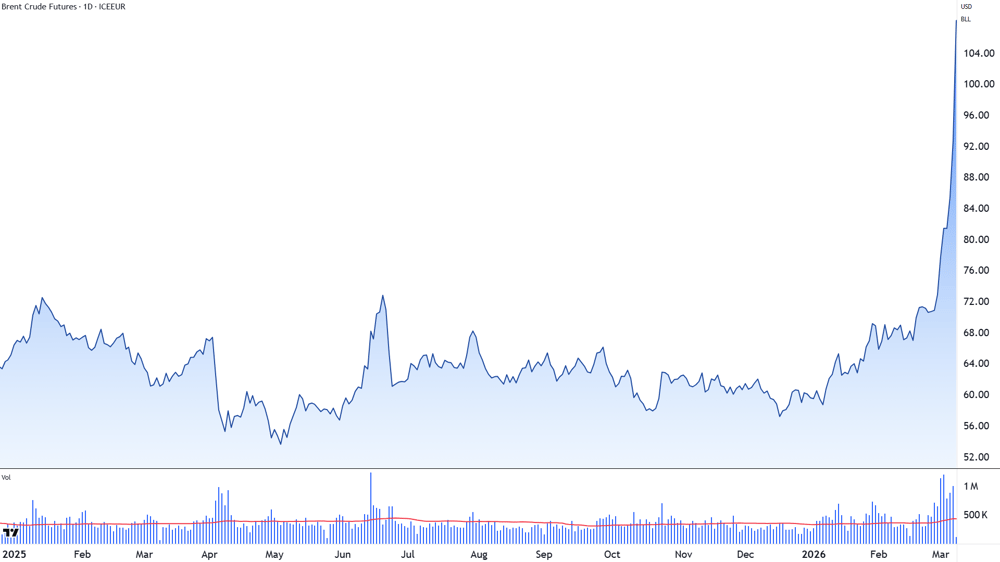

Oil Prices Breach Key Thresholds

The benchmark Brent crude oil spot price has surged past the US$100 per barrel mark, even briefly touching US$109 in early trading. This represents the highest level seen since March 2022, a period marked by significant energy market volatility following Russia’s invasion of Ukraine. Such substantial price movements are typically indicative of major geopolitical stress, underscoring the seriousness with which the market is treating the current developments.

Brent Crude Oil Futures chart since 1 Jan 2025

ASX Faces Steep Decline, Energy Sector Shines

In Australia, the ASX 200 index has mirrored the global trend, plummeting approximately 4% in early trade. This marks the most significant single-day drop for the benchmark since the period of escalating trade tariffs in April of last year, and prior to that, the severe market downturn experienced during the initial phases of the COVID-19 pandemic. The prevailing sentiment among investors is a pronounced shift away from riskier assets, as the prospect of higher energy costs looms, threatening to dampen global economic growth and compress corporate profit margins.

However, amidst this broad market downturn, a specific sector has emerged as a beacon of strength. The energy sector is experiencing a remarkable surge, with the spike in oil prices almost instantaneously transforming the earnings outlook for companies involved in the production, refining, and export of crude oil and petroleum products. For these businesses, each incremental increase in the oil price can directly translate into enhanced cash flow.

For investors seeking to capitalise on this momentum, the Australian Securities Exchange (ASX) energy sector has suddenly regained prominence. The critical question for many is which ASX-listed companies are best positioned to benefit from the escalating oil prices, and whether their current valuations already reflect this anticipated upside.

This analysis delves into the major ASX-listed oil and downstream energy companies, examining their operational strengths and how each entity is poised to gain from the current surge in crude oil prices. We will also review the latest broker research, including consensus ratings and price targets, to provide an indication of how analysts perceive these stocks in the evolving oil price environment.

The ASX Stocks Poised to Profit from Crude Oil Volatility

The current surge in oil prices is fundamentally driven by concerns over supply. Heightened conflict involving Iran has led to the effective shutdown of vessel transit through the Strait of Hormuz, a critical global oil shipping artery. This development has compelled traders to rapidly reassess the probability of sustained disruptions to global crude oil and liquefied natural gas (LNG) flows.

Consequently, the spotlight is firmly fixed on ASX-listed oil and gas producers, as well as downstream refiners and retailers. The companies highlighted below are those already engaged in production, positioning them to capture the immediate benefits of higher crude and LNG prices, rather than those with projects requiring years of development. They are presented in descending order of market capitalisation.

Woodside Energy (WDS)

Market Capitalisation: $58.5 billion

Woodside Energy (WDS) chartCore Operations:

- Pluto LNG (Western Australia): Woodside operates and holds a 90% stake in this LNG facility in the Pilbara region. It processes offshore gas from the Pluto and Xena fields into LNG, also providing domestic gas and trucked LNG.

- North West Shelf Project (Western Australia): As operator, Woodside holds an aggregate interest of 33.33% across most joint ventures within this major LNG and domestic gas hub in the Pilbara, serving both Australian and export markets.

- Sangomar (offshore Senegal): Woodside is the operator of Senegal’s inaugural major oil project, holding an 82% interest in the Sangomar exploitation area. This offshore field, located approximately 100 kilometres south of Dakar, is focused on oil production.

Production: Woodside reported a record group-level production of 198.8 million barrels of oil equivalent for the full year 2025, bolstered by strong output from Sangomar and high operational reliability at its LNG assets.

Dividend Yield: Based on a trailing 12-month dividend payout of $1.653 per share and a closing price of $30.75 on Friday, March 6, Woodside Energy’s dividend yield stands at 5.3% per annum. Its two most recent dividends were fully franked.

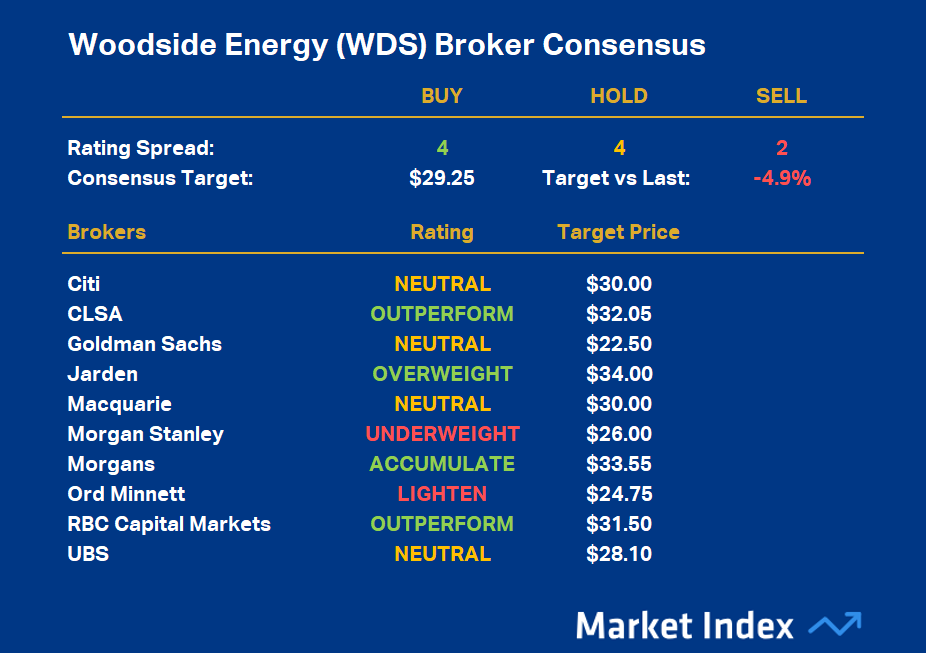

Broker Consensus:

Woodside Energy Broker Consensus

Woodside Energy’s Broker Consensus Rating is +0.2, indicating a HOLD recommendation. The average Broker Consensus Target price is $29.25. This suggests that, on average, brokers believe the stock is approximately 4.9% overvalued relative to its closing price of $30.75 on Friday, March 6.

Santos (STO)

Market Capitalisation: $24.2 billion

Santos (STO) chartCore Operations:

- Gladstone LNG (Queensland, Australia): Santos operates this coal seam gas-to-LNG export project on Curtis Island, holding a 30% interest. The project is supplied by gas from the Bowen and Surat basins.

- PNG LNG (Papua New Guinea): Santos holds a 42.5% interest in this ExxonMobil-operated LNG project, which exports gas to Asian markets.

- Darwin LNG / Barossa (Northern Territory, Australia): Santos is the operator with approximately 50% ownership of the Barossa gas field. This field is slated to supply the Darwin LNG plant as the existing Bayu-Undan field’s production declines.

- Pikka Phase 1 (Alaska, USA): Santos possesses a 51% stake in this oil development on Alaska’s North Slope, with first production anticipated in the mid-2020s.

Production: Santos reported full-year 2025 production of 87.7 million barrels of oil equivalent (mmboe), near the upper end of its guidance.

Dividend Yield: Based on a full-year dividend of $0.348 per share for 2025 and a closing price of $7.46 on Friday, March 6, Santos’s dividend yield is 4.6% per annum. Its last two dividends averaged 5% franking.

Broker Consensus:

Santos Broker Consensus

Santos’s Broker Consensus Rating is +0.8, indicating a BUY recommendation. The average Broker Consensus Target price is $7.75. This suggests that, on average, brokers believe the stock is approximately 3.9% undervalued relative to its closing price of $7.46 on Friday, March 6.

Origin Energy (ORG)

Market Capitalisation: $20.6 billion

Origin Energy (ORG) chartCore Operations:

- Australia Pacific LNG (Queensland, Australia): Origin holds a 27.5% interest in this coal seam gas-to-LNG export project, operated by ConocoPhillips. The gas is sourced from the Surat and Bowen basins and exported via the Curtis Island LNG facility near Gladstone.

- Integrated Energy Business (Australia): Origin also manages a substantial portfolio of electricity and gas retail operations, alongside power generation assets across Australia’s National Electricity Market.

Production: Origin Energy’s share of production from Australia Pacific LNG was approximately 69 petajoules of gas in FY2025, representing its primary upstream energy production exposure.

Dividend Yield: Based on Origin Energy’s trailing 12-month dividend payout of $0.60 per share and a closing price of $11.94 on Friday, March 6, its dividend yield is 3.7%. Its two most recent dividends were fully franked.

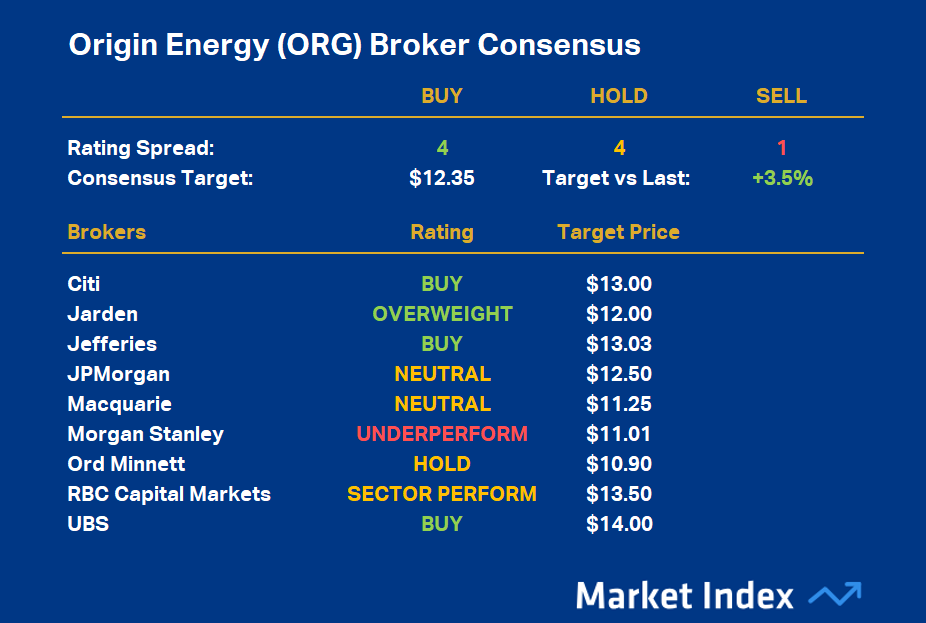

Broker Consensus:

Origin Energy Broker Consensus

Origin Energy’s Broker Consensus Rating is +0.33, indicating a HOLD recommendation. The average Broker Consensus Target price is $12.35. This suggests that, on average, brokers believe the stock is approximately 3.5% undervalued relative to its closing price of $11.94 on Friday, March 6.

Ampol (ALD)

Market Capitalisation: $7.4 billion

Ampol (ALD) chartCore Operations:

- Lytton Refinery (Queensland, Australia): Ampol owns and operates this significant fuel refinery in Brisbane, one of Australia’s last remaining facilities. It produces petrol, diesel, jet fuel, and other refined petroleum products.

- Fuel Supply and Retail Network (Australia and New Zealand): Ampol manages an extensive fuel import, distribution, and retail network, supplying transport fuels through a national network of service stations and to commercial fuel clients.

- Z Energy (New Zealand): Ampol holds 100% ownership of Z Energy, a leading fuel distributor and retailer of petrol, diesel, and aviation fuels across New Zealand.

Production: Ampol’s Lytton refinery processes approximately 109,000 barrels of crude oil daily, supplying refined transport fuels to the domestic market.

Dividend Yield: Based on Ampol’s trailing 12-month dividend payout of $1.00 per share and a closing price of $30.96 on Friday, March 6, its dividend yield is 3.2%. Its two most recent dividends were fully franked.

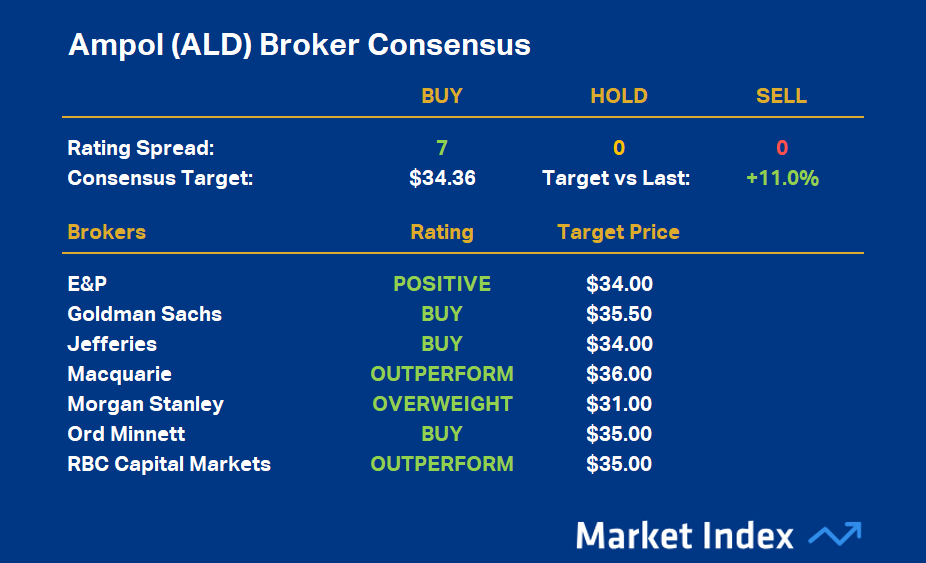

Broker Consensus:

Ampol Broker Consensus

Ampol’s Broker Consensus Rating is +1.0, indicating a BUY recommendation. The average Broker Consensus Target price is $34.36. This suggests that, on average, brokers believe the stock is approximately 11.0% undervalued relative to its closing price of $30.96 on Friday, March 6.

Viva Energy (VEA)

Market Capitalisation: $7.4 billion

Viva Energy (VEA) chartCore Operations:

- Geelong Refinery (Victoria, Australia): Viva Energy owns and operates Australia’s second remaining oil refinery. It processes crude oil into petrol, diesel, jet fuel, and other refined products for the domestic market.

- Fuel Supply and Retail Network (Australia): Viva Energy imports, distributes, and markets fuels across Australia via a national network of fuel distribution and retail sites, notably including its long-standing Shell-branded service station network.

- Commercial Fuels and Aviation (Australia): Viva Energy is a major supplier of aviation and commercial fuels, serving airports, transport operators, and industrial clients nationwide.

Production: Viva Energy’s Geelong refinery processes around 120,000 barrels of crude oil per day, primarily supplying refined fuels to the Australian market.

Dividend Yield: Based on Viva Energy’s trailing 12-month dividend payout of $0.067 per share and a closing price of $2.10 on Friday, March 6, its dividend yield is 3.2%. Its two most recent dividends were fully franked.

Broker Consensus:

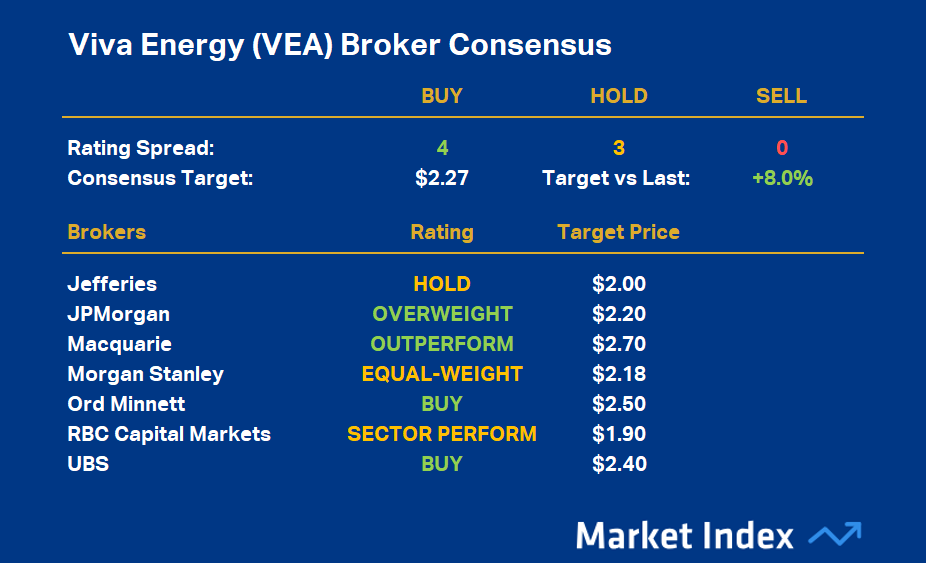

Viva Energy Broker Consensus

Viva Energy’s Broker Consensus Rating is +0.57, indicating a BUY recommendation. The average Broker Consensus Target price is $2.27. This suggests that, on average, brokers believe the stock is approximately 8.0% undervalued relative to its closing price of $2.10 on Friday, March 6.

Beach Energy (BPT)

Market Capitalisation: $2.6 billion

Beach Energy (BPT) chartCore Operations:

- Western Flank Oil Fields (Cooper Basin, Australia): Beach holds a 100% interest in several producing oil fields within the South Australian Cooper Basin, which are a primary source of the company’s oil output.

- Waitsia Gas Project (Perth Basin, Western Australia): Beach holds a 50% interest in the Waitsia gas field and its Stage 2 development, alongside operator Mitsui E&P Australia. Gas from Waitsia is processed at the Waitsia Gas Plant for the domestic market.

- Otway Basin Gas Assets (Victoria and South Australia): Beach operates and holds significant interests in multiple offshore and onshore gas fields, supplying gas to the Australian east coast market.

Production: Beach Energy reported FY2025 production of approximately 20.2 million barrels of oil equivalent at the group level, derived from its Cooper, Otway, and Perth Basin assets.

Dividend Yield: Based on Beach Energy’s trailing 12-month dividend payout of $0.07 per share and a closing price of $1.15 on Friday, March 6, its dividend yield is 6.1%. Its two most recent dividends were fully franked.

Broker Consensus:

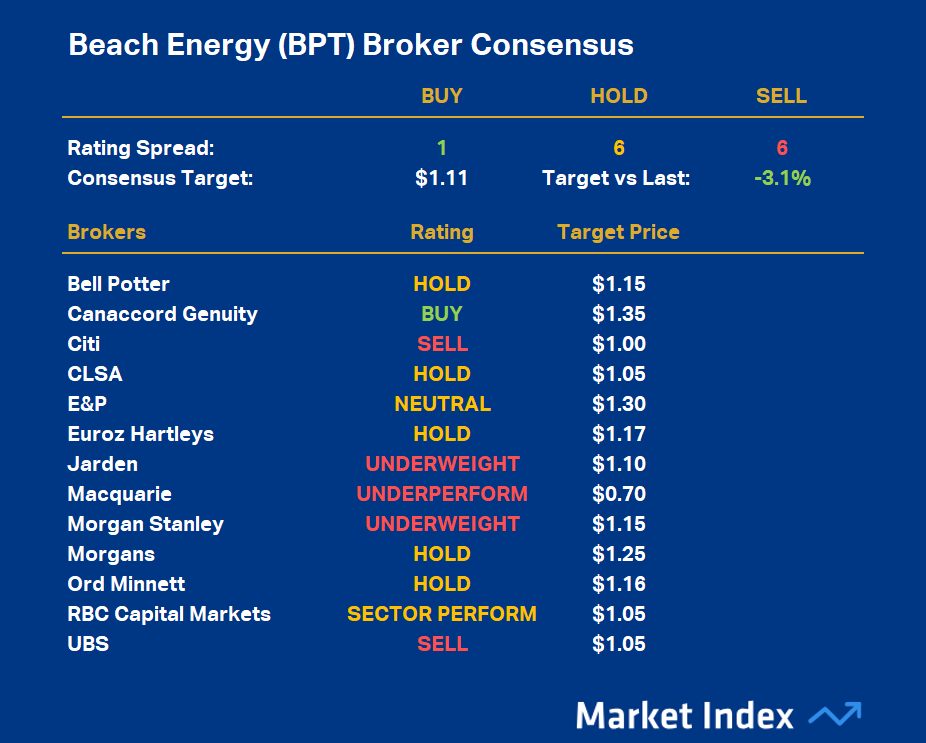

Beach Energy (BPT) Broker Consensus

Beach Energy’s Broker Consensus Rating is -0.38, indicating a HOLD recommendation. The average Broker Consensus Target price is $1.11. This suggests that, on average, brokers believe the stock is approximately 3.1% overvalued relative to its closing price of $1.15 on Friday, March 6.

Karoon Energy (KAR)

Market Capitalisation: $3.4 billion

Karoon Energy (KAR) chartCore Operations:

- Baúna Oil Field (Santos Basin, Brazil): Karoon holds a 100% interest in this offshore oil project, located approximately 210 kilometres off the coast of Brazil. Production is managed via the FPSO Cidade de Itajaí, with crude exported to international markets.

- Patola Field (Santos Basin, Brazil): Karoon possesses a 100% interest in the Patola oil field, a subsea tie-back development that utilises the Baúna infrastructure for production.

- Neon Project (Brazil): Karoon holds a 100% interest in the Neon offshore oil discovery within the Santos Basin, which is currently under assessment for potential future development.

Production: Karoon Energy reported 2025 production of approximately 9.8 million barrels of oil equivalent, primarily from the Baúna and Patola fields in Brazil.

Dividend Yield: Karoon Energy does not currently pay a dividend, as its cash flows are largely reinvested into development and exploration activities.

Broker Consensus:

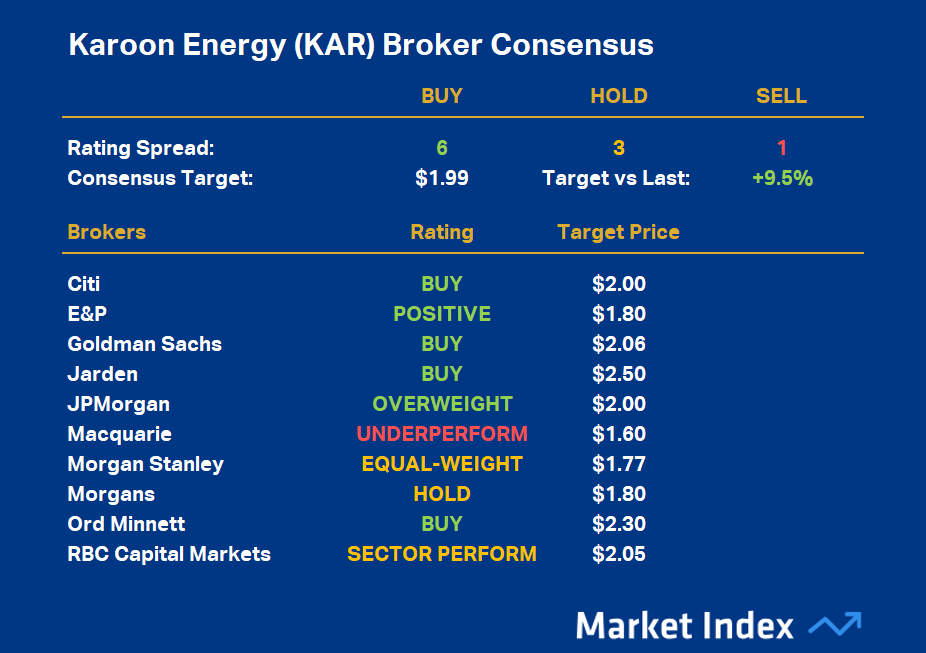

Karoon Energy Broker Consensus

Karoon Energy’s Broker Consensus Rating is +0.50, indicating a BUY recommendation. The average Broker Consensus Target price is $1.99. This suggests that, on average, brokers believe the stock is approximately 9.5% undervalued relative to its closing price of $1.815 on Friday, March 6.

Amplitude Energy (AEL)

Market Capitalisation: $786 million

Amplitude Energy (ALD) chartCore Operations:

- Sole Gas Project (Gippsland Basin, Australia): Amplitude Energy holds a 100% interest in the Sole offshore gas field, situated in the Gippsland Basin off the coast of Victoria. Gas is processed at the Orbost Gas Processing Plant and supplied to the east coast domestic gas market.

- East Coast Gas Portfolio (Australia): The company also holds interests in several offshore Gippsland Basin exploration and appraisal permits, targeting future domestic gas supply opportunities.

Production: Amplitude Energy reported FY2025 production of approximately 9.0 petajoules of gas, primarily sourced from the Sole gas field supplying the east coast market.

Dividend Yield: Amplitude Energy does not currently pay a dividend, with its cash flows focused on supporting operations and maintaining balance sheet strength.

Broker Consensus:

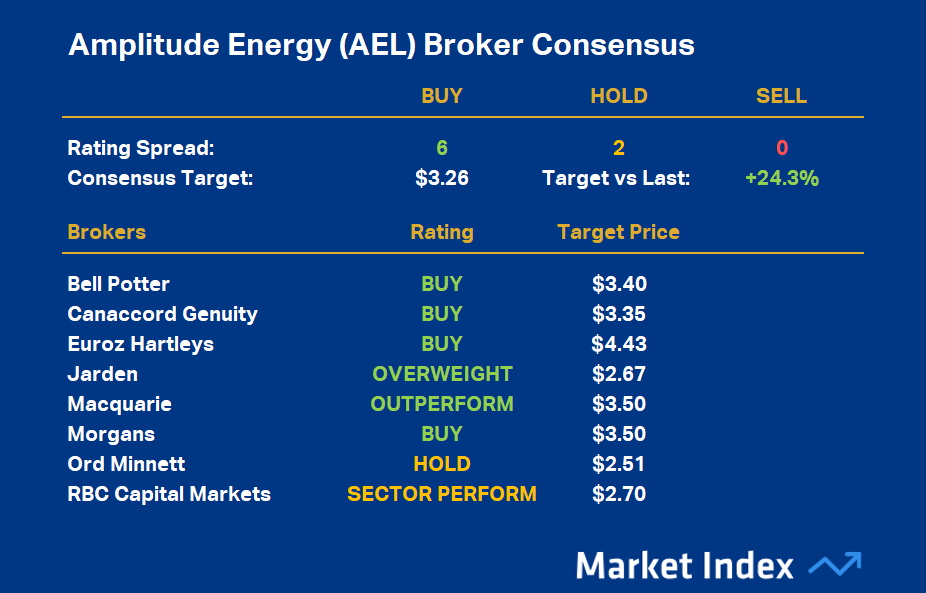

Amplitude Energy Broker Consensus

Amplitude Energy’s Broker Consensus Rating is +0.75, indicating a BUY recommendation. The average Broker Consensus Target price is $3.26. This suggests that, on average, brokers believe the stock is approximately 24.3% undervalued relative to its closing price of $2.62 on Friday, March 6.

{kind=link}