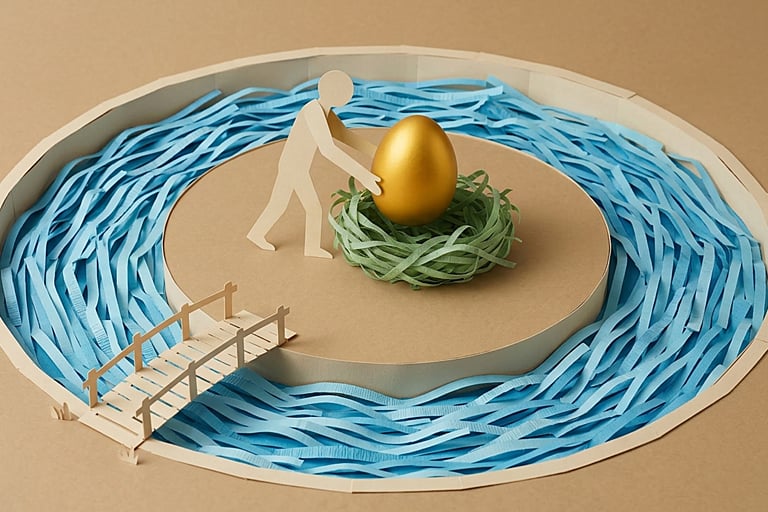

Retirement Dreams: Australians Eye $1 Million Mark Amidst Growing Financial Anxiety

The conversation around retirement in Australia is a potent barometer of the nation’s financial sentiment. While the specific dollar figure Australians believe they need for a comfortable retirement might seem like a simple projection, it offers a profound glimpse into current economic anxieties and future financial confidence, or lack thereof. Recent findings from Colonial First State’s (CFS) “Rethinking Retirement 2026” report highlight a significant shift, with the average Australian now believing a cool $1 million is the benchmark for a “comfortable” retirement.

This figure alone is substantial, but the context of a staggering $183,000 surge in this perceived requirement within just the last year paints a more concerning picture. It strongly suggests that Australians are experiencing a considerable dip in confidence regarding their ability to maintain their desired lifestyle once they step away from the workforce. While inflation has undoubtedly been a persistent challenge, a year-on-year increase of 22% in the perceived retirement nest egg seems to outpace the actual rise in living costs, pointing towards deeper-seated financial unease.

Kelly Power, CFS’s Chief Executive Officer for Superannuation, emphasises that retirement transcends mere financial adjustments. “For many Australians, it brings a range of questions and considerations – from whether savings will be enough, to how to navigate an increasingly complex system,” Power explains. “Retirement is not a universal or linear experience. It is deeply personal, and so are the questions people bring to it.”

The Shadow of FORO: Fear of Running Out in Retirement

Financial advisers often encounter a prevalent concern among those nearing retirement: the “Fear of Running Out” (FORO). This anxiety is particularly acute for individuals lacking confidence in their financial standing and appears to transcend socio-economic divides. People become accustomed to a particular standard of living and worry about its preservation, irrespective of their earning capacity.

Robert Rich, Director and Financial Adviser at Unite Wealth, observes that many clients tend to overestimate the capital required for a comfortable retirement. “They will either assume they need to work longer or save up a larger nest-egg. I find that clients usually omit four major elements that play a significant role in funding their living expenses after work,” Rich notes.

Key Overlooked Retirement Funding Elements:

- Compounding Growth: A common oversight is forgetting that invested funds continue to grow during retirement. Clients often perform a simple calculation: “$1 million in super, spending $100,000 each year means their super will only last for 10 years.” This ignores the crucial impact of ongoing investment returns.

- Government Age Pension: For many households, the age pension provides a substantial portion of their living expenses, typically between one-third and half. This significantly reduces the reliance on personal superannuation and investment withdrawals.

- Inheritances: The potential impact of a future inheritance is frequently underestimated. Receiving proceeds from an estate can be transformative, potentially enabling individuals to retire or significantly reduce their working hours five to ten years earlier than anticipated.

- Home Equity and Reverse Mortgages: For those without dependents or who wish to utilise their inheritance during their lifetime, reverse mortgages offer a viable option. By leveraging the equity in their homes, individuals can subsidise their living expenses, thereby requiring a smaller overall nest egg.

While Rich often uses the ASFA Retirement Standard as a reference point for his clients, he acknowledges that the “correct amount” exists on a spectrum, highly dependent on individual circumstances. The recent $183,000 jump in perceived needs, he suggests, is likely influenced by geopolitical events, such as the conflict in Iran, and rising interest rates, which collectively foster negative sentiment. “It’s a huge jump over a 12-month period, but the news cycle has been littered with bad news pretty consistently over recent months and this would lead to a lack of confidence in their savings lasting,” he posits.

Navigating the Path to a Secure Retirement

For investors feeling the pressure to reach a specific retirement target, whether it’s the sentiment-driven $1 million or ASFA’s benchmark of $730,000 for a couple, Rich advises against succumbing to excessive stress.

Strategies for a Healthier Retirement Outlook:

- Diversify Assets: Beyond superannuation, families should consider the value of other investments and family businesses, which can significantly bolster retirement funding strategies.

- Maximise Tax-Effective Contributions: Utilising tax-deductible superannuation contributions is a powerful method for accelerating retirement savings.

- Explore Multiple Investment Avenues: Pursuing diverse investment opportunities, such as share portfolios or investment properties, acts like adding dedicated team members to your financial strategy, working to grow wealth annually. The principle of “many hands make light work” applies here, amplified by the long-term benefits of compound returns.

- Understand and Manage Investment Risk: A critical, yet often overlooked, aspect is understanding investment risk, particularly “sequencing risk” – the danger of a market downturn occurring early in retirement. Many individuals are unaware of the risks embedded in their superannuation strategies and can become overly confident, especially after periods of strong market performance. Rich warns that a significant market correction could rapidly diminish substantial superannuation balances.

Depending on an individual’s risk tolerance and life stage, a more conservative investment approach might be warranted. “Families would be encouraged to look at the investment options they are currently invested in and consider if they would feel comfortable during a market correction,” Rich advises. For those with substantial balances nearing retirement, “building a moat around your retirement nest-egg and taking the more conservative, safe or boring path moving forward” may be prudent. While perhaps not as thrilling, this measured approach can ultimately lead to a more comfortable and secure retirement.

{kind=link}