US Economic Data: A Weekend of Surprises and Skepticism

The recent economic data released in the United States over the weekend has certainly provided plenty to ponder, even for those who might not typically find economic figures “interesting.” This past week has seen a fascinating interplay between inflation reports, job market revisions, and market reactions, prompting questions about the accuracy and interpretation of the numbers we’re seeing.

Inflation Figures: Welcome, But Not a Game Changer

On Friday, the Consumer Price Index (CPI) data for January was released, showing inflation came in at a less-than-expected 2.4% year-on-year. Core inflation, which excludes volatile food and energy prices, stood at 2.5% for the 12 months ending January.

On the surface, this cooler inflation reading might suggest that the U.S. Federal Reserve could be more inclined to cut interest rates at its upcoming meeting. A lower inflation rate typically reduces the pressure on central banks to maintain higher interest rates to curb price increases. However, the market’s reaction thus far has been muted.

U.S. stock futures remained relatively flat following the inflation announcement, even with a U.S. holiday on Monday impacting trading volumes. This suggests that investors aren’t yet convinced that the inflation data will be a strong catalyst for an immediate rate cut.

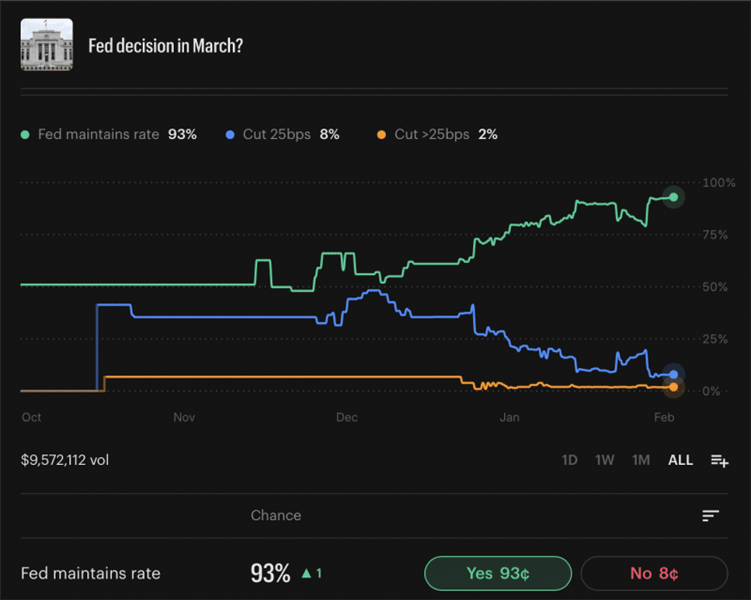

Furthermore, looking at prediction markets, the sentiment regarding a March rate cut hasn’t significantly shifted. On the Kalshi platform, the odds of a rate cut in March remained largely unchanged, with the overwhelming majority still favouring a pause by the Fed. Only a small percentage of traders, around 8%, anticipate a 25 basis point (bps) cut. This figure saw only a marginal increase from 7% the previous Thursday.

A more closely watched indicator, the CME Group’s FedWatch tool, also reflects this cautious outlook. As of Monday afternoon, the tool priced in a 90.2% chance of the Federal Reserve holding interest rates steady. This is only a slight decrease from the 93.6% probability of a hold observed last Thursday. The lack of a significant shift in these indicators points to a prevailing belief that the Fed will likely maintain its current monetary policy stance for the time being.

The Shocking Jobs Revision: A Twenty-Year Low

Perhaps the most significant economic news to emerge was the substantial downward revision to U.S. jobs data, the largest in two decades. It has been revealed that across the 2025 calendar year, an estimated 1,029,000 jobs that were initially counted did not, in fact, exist. This means the U.S. labour market experienced its largest downward revision in job numbers in twenty years. This follows previous downward revisions of 818,000 roles in 2024 and a negative revision of 306,000 in 2023, indicating a concerning trend of overestimation in job figures.

Over the past three years, the cumulative downward revision of jobs data has exceeded 2.15 million. In essence, this means that for the last three years, over 2.15 million jobs that were initially reported as existing were later found to be non-existent when more accurate data became available.

When one considers the magnitude of these job revisions alongside the performance of major U.S. stock indices like the S&P 500, NASDAQ, and even the Dow Jones over the same three-year period, it begins to shed light on why Wall Street might appear indifferent to the latest economic data. The consistent upward trend in equity markets, despite these significant discrepancies in labour market reporting, suggests that investors may be looking beyond traditional economic indicators or perhaps have grown accustomed to a certain level of data “massage.”

The discrepancy between reported job numbers and the actual figures raises important questions about the methodology and accuracy of economic data collection and reporting. While the Federal Reserve may look at a range of indicators, the sheer scale of these revisions could introduce uncertainty into economic forecasting and policy decisions.

Key Takeaways from the Weekend’s Data:

- Inflation is cooling, but not dramatically: January’s CPI figures were below expectations, but the market reaction suggests it’s not yet a strong enough signal for an immediate Fed rate cut.

- Rate cut expectations remain cautious: Prediction markets and the FedWatch tool indicate a strong likelihood of the Federal Reserve holding interest rates steady at its next meeting.

- Massive jobs revision shakes confidence: The largest downward revision to U.S. jobs data in 20 years raises concerns about the accuracy of labour market reporting.

- Wall Street’s apparent indifference: The strong performance of stock markets despite data revisions suggests a potential disconnect between reported economic realities and investor sentiment.

The ongoing analysis of U.S. economic data highlights the complexities of interpreting financial information and the potential for surprising revisions to reshape our understanding of the economy. As always, investors are encouraged to conduct their own thorough research and consult with qualified financial advisors before making any investment decisions.

{kind=link}